All about Sukanya Samriddhi Account

Keeping in the theme of “Beti Bachao Beti Padhao” i.e. all round development of Girl child, the Government of India has launched Sukanya Samriddhi Account – a long term deposit scheme for girl child.

The post covers everything you wanted to know about the new investment avenue.

1. Who can open the account?

This account can be opened only for girl child who is below 10 years of age (as of account opening date) by their natural or legal guardian. One year relaxation is available for this year, which means even if the child has turned 10 anytime in 2014, you can still open this account in her name.

The account can only be opened for 2 girl children. Third account can be opened in exceptional cases where the depositor was blessed with 3 girl children at the first birth or twin girl children at the second birth.

Also Read: PPF – A Must Have Investment

2. Where can the account be opened?

The account can be opened in most public sector banks and Post offices.

I personally would advise going to large public sector banks like SBI as they are more advanced in terms of online access etc. As this is new investment avenue most banks would not have online access in place, but going forward larger banks would be first to bring those accounts online thereby giving convenience as it happened in case of PPF.

Moreover, the account can be transferred anywhere in India.

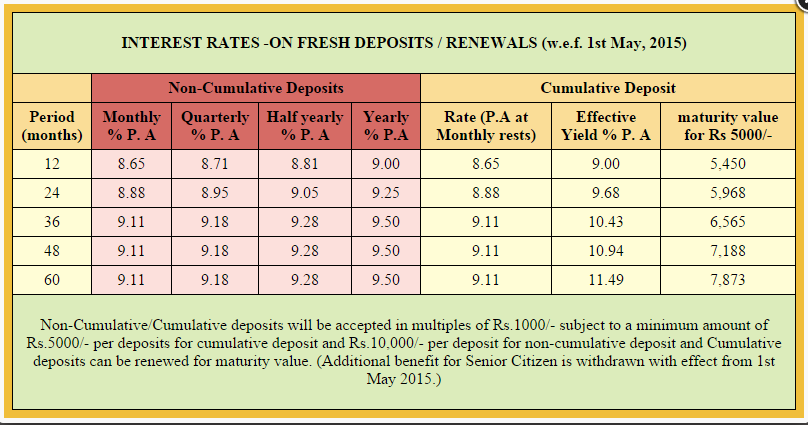

3. How much interest would be paid?

The interest would be paid annually and would be notified every year by Government of India like in case of PPF.

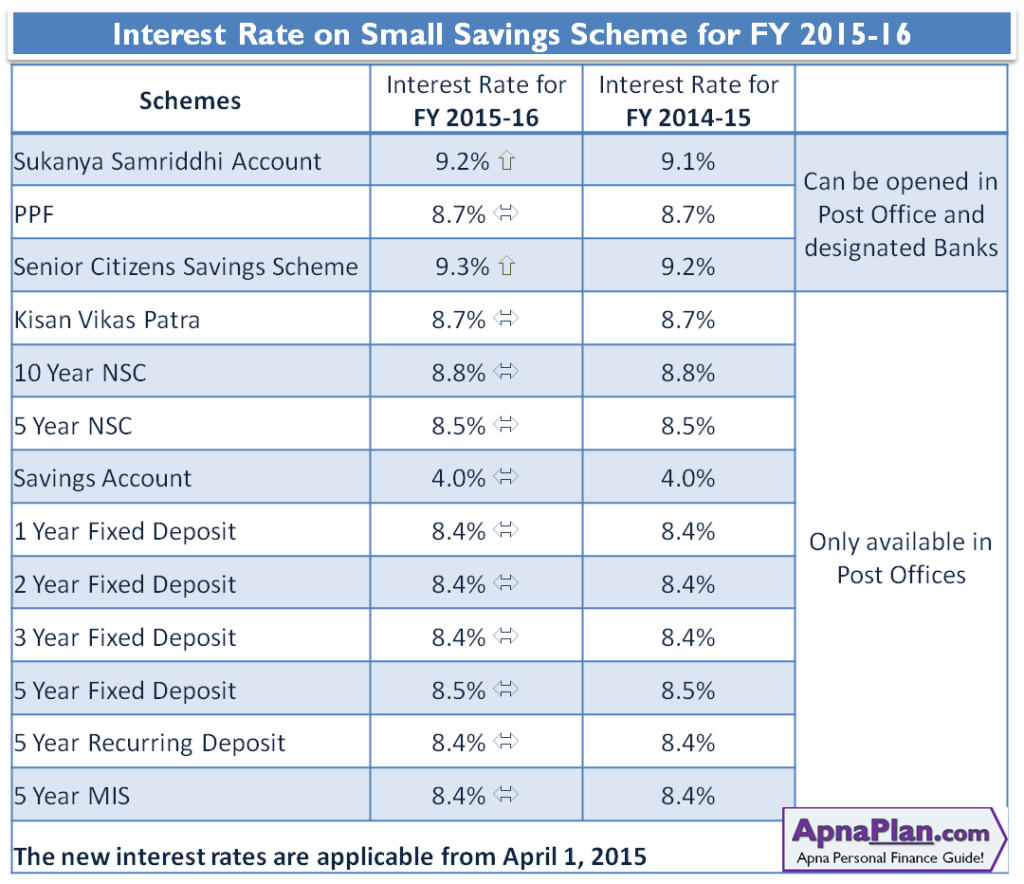

For Financial year 2014-15 its 9.1%.

4. What are the documents required?

You would require the following documents for opening of account:

- Date of Birth proof for the child

- Your Identity Proof

- Your Address Proof

These are regular KYC documents that you require for opening a new bank account.

5. Rules for Deposit?

The account can be opened with minimum deposit of Rs 1,000 and multiples of Rs 100 thereafter. The maximum amount that can be deposited in the account is Rs 1.5 lakhs every financial year.

The deposit has to be made in cash, cheque or demand draft. Online option might be available in future as banks connect this with core banking.

Also minimum deposit of Rs 1,000 needs to be made every financial year; else a penalty of Rs 50 would be levied.

6. Premature withdrawal?

Depositors can withdraw 50% of the balance after the girl child turns 18 for higher education or marriage only.

7. Account Maturity?

The deposit has to be made for first 14 years from the year of account opening. The account matures either from 21 years from the date of account opening or when the girl is married, whichever is earlier.

Account would be closed prematurely in event of death of the girl child.

8. Loan Facility?

There is NO loan facility under this scheme.

9. Taxation?

Budget 2015 has made taxation of Sukanya Samriddhi Account EEE – i.e, “Exempt”,”Exempt”,”Exempt”. This means that the amount deposited up to Rs 1.5 lakh gives tax exemption u/s 80C.

Moreover there is no tax on interest received in the account and also there is no tax on withdrawal at maturity.

Recommendation:

Sukanya Samriddhi Account is a good initiative from Government to secure the future of girl child. Also the offer of higher interest rates than PPF is a welcome proposition.

Also Budget 2015 has made the product tax free at the time of maturity which is similar to PPF. So in most cases Sukanya Samriddhi Account is better alternative to PPF for girl child. This said you should also look to equity mutual funds for planning your child’s future.